Does Insurance Cover Medical Tourism? What You Need to Know Before You Travel

Dec, 26 2025

Dec, 26 2025

When you hear the term medical tourism, you might picture someone flying to Thailand for a dental crown or India for a heart bypass. But here’s the real question most people don’t ask until it’s too late: Will my insurance pay for it? The answer isn’t yes or no-it’s complicated, and getting it wrong can cost you thousands.

Most Domestic Insurance Plans Don’t Cover Medical Tourism

If you’re covered by a UK NHS plan, Medicare in the US, or a standard private health plan in Canada or Australia, you’re almost certainly not covered for treatment abroad. These plans are built around local networks. They negotiate prices with hospitals and doctors in your home country. Once you step outside those borders, your insurer sees you as a foreign patient-and that’s not part of their contract.There are exceptions. A few high-end private insurers in the UK and US offer international coverage as an add-on, but they’re rare and expensive. Even then, they usually require pre-approval. You can’t just book a flight to Mexico for a knee replacement and expect reimbursement afterward.

Why Insurers Say No

Insurance companies aren’t being stubborn. They have real risks to manage. When you get surgery overseas, they lose control over three key things: quality, cost, and continuity.Quality-They can’t verify if the hospital meets their safety standards. A clinic in Tijuana might be clean and licensed, but does it have the same infection control protocols as a hospital in Birmingham? Insurers can’t audit every facility worldwide.

Cost-Overseas procedures often cost less because wages, rent, and regulations are lower. But if insurers started paying for those, they’d have to renegotiate all their domestic contracts. A $10,000 hip replacement in India could force a UK hospital to drop its $25,000 price-or lose patients.

Continuity-What if you have complications after you return home? Your local doctor didn’t perform the surgery. They don’t have your medical records. They don’t know the implant brand or the surgeon’s technique. Who’s responsible when something goes wrong?

What Insurance Might Cover-If Anything

There are a few narrow cases where your insurance might help:- Emergency care abroad-If you’re traveling and have a heart attack, most travel insurance policies will cover emergency treatment. But that’s not medical tourism. That’s an accident.

- Pre-authorized experimental treatments-A few insurers will cover experimental or off-label procedures if they’re not available in your country and you have documented clinical need. This requires months of paperwork and specialist reviews.

- Corporate wellness programs-Some large employers offer overseas treatment as a benefit. Google, Apple, and a few UK-based firms have done this for employees needing faster access to specialists.

Don’t assume you’re covered. Always call your insurer and ask: “If I travel to [country] for [procedure], will you pay for it?” Record the name of the person you speak to and their reference number. Get it in writing.

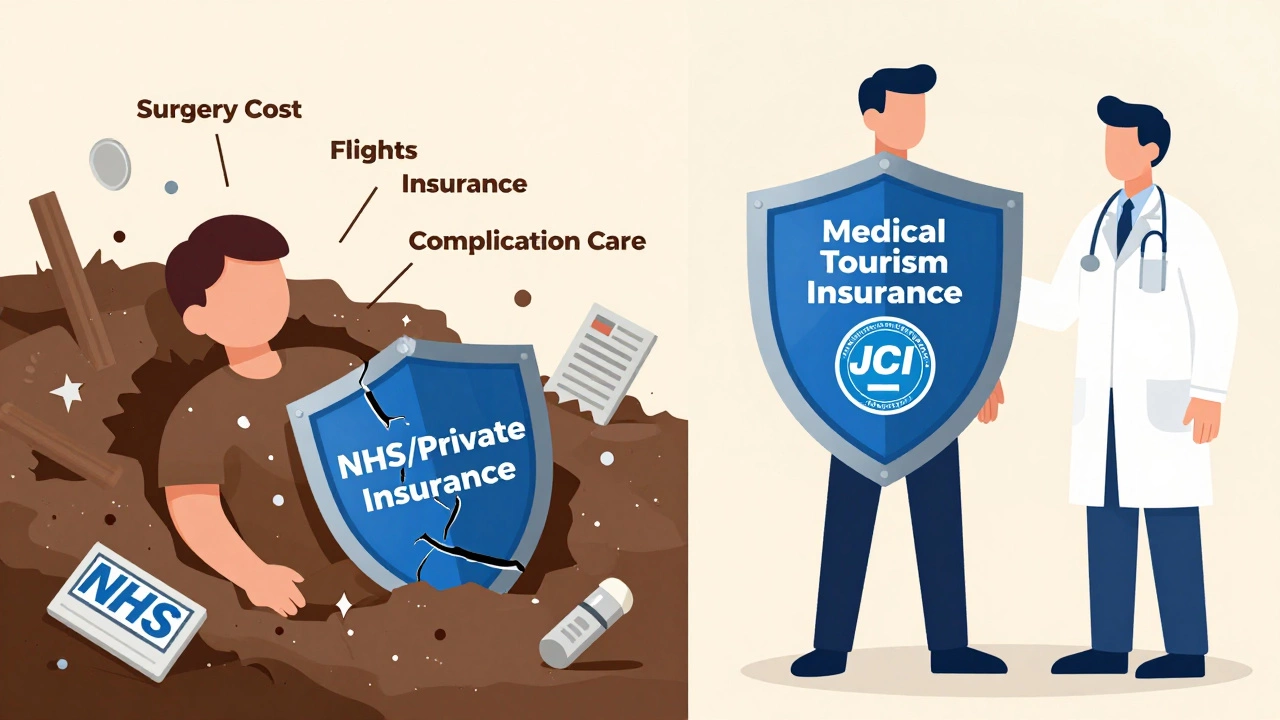

Medical Tourism Insurance: A Separate Product

If you’re serious about going overseas for treatment, you need a different kind of insurance: medical tourism insurance. This isn’t travel insurance. It’s a specialized policy designed for people seeking planned care abroad.These policies typically cover:

- Complications from the procedure (up to 90 days after surgery)

- Emergency return flights if something goes wrong

- Additional accommodation for you or a companion

- Lost deposits if your surgery is canceled

- Medical record transfer between countries

Companies like MedTrip Insurance, Global Health Insurance, and Allianz Travel offer these plans. Prices vary based on the procedure, your age, and destination. For a $15,000 spinal fusion in Thailand, expect to pay $800-$1,500 for full coverage.

Read the fine print. Some policies exclude pre-existing conditions. Others won’t cover you if you go to a country under government travel advisories (like Venezuela or Sudan). Some only cover procedures at hospitals they’ve pre-approved.

What Happens When Things Go Wrong

Let’s say you had a hip replacement in Hungary for $8,000 and returned home. Two weeks later, you develop an infection. Your UK GP says you need IV antibiotics and a second surgery.If you didn’t buy medical tourism insurance, you’re on your own. The Hungarian clinic might offer a refund or free revision-but only if you’re still there. Once you’re back in the UK, they’re not legally responsible. Your NHS won’t cover the revision because you chose to go abroad. Your private insurer won’t pay because it wasn’t approved.

This isn’t hypothetical. In 2024, the UK’s National Health Service reported over 300 cases of patients returning with complications from overseas procedures. Many had to be treated at public expense because they had no coverage.

How to Protect Yourself

If you’re considering medical tourism, here’s how to avoid disaster:- Verify the hospital-Look for accreditation from JCI (Joint Commission International) or similar global bodies. Avoid clinics with no public accreditation.

- Get your records-Before you leave, get a full copy of your medical history and send it to your home doctor. Keep digital and paper copies.

- Buy medical tourism insurance-Don’t rely on travel insurance. Get a policy that covers complications, not just lost luggage.

- Plan for follow-up-Ask the overseas clinic if they’ll provide post-op guidance. Ask your home doctor if they’ll take you back as a patient after the procedure.

- Know the legal limits-In most countries, you can’t sue a foreign hospital easily. Your rights are limited. Insurance is your real safety net.

Is Medical Tourism Worth the Risk?

For some, the answer is yes. A liver transplant in India might cost $40,000 instead of $300,000 in the US. A dental implant in Poland can be 70% cheaper than in the UK. For people without insurance, or those stuck on long waiting lists, it’s the only option.But it’s not a bargain if you end up paying twice. You pay the clinic upfront. You pay for flights and accommodation. You pay for insurance. And if something goes wrong, you pay again for emergency care at home.

The real savings come when you plan carefully. Choose accredited facilities. Get insurance. Talk to your doctor. Don’t let price be the only factor.

Alternatives to Medical Tourism

Before you book a flight, consider other options:- Domestic waiting list programs-The UK NHS offers some patients the option to be treated at another NHS hospital with shorter waits.

- Private insurance upgrades-Some UK insurers let you pay extra to reduce waiting times for non-emergency care.

- Payment plans-Many UK hospitals offer 0% financing for major procedures.

- Telemedicine consultations-Get a second opinion from a specialist abroad without leaving home. Some US and German doctors offer remote reviews for under $300.

These won’t save you 80%, but they’ll keep you safe-and covered.

Does the NHS cover medical tourism?

No, the NHS does not cover treatment abroad unless it’s an emergency or pre-approved under very rare circumstances. If you choose to go overseas for non-emergency care, you’re responsible for all costs, including complications after you return.

Can I use my private health insurance for overseas surgery?

Most private insurers in the UK won’t cover overseas procedures unless you get written pre-approval. Even then, they usually only pay if the treatment is unavailable in the UK and deemed medically necessary. Always call your insurer and ask for confirmation in writing.

What’s the difference between travel insurance and medical tourism insurance?

Travel insurance covers accidents, lost bags, and emergency care while you’re abroad. Medical tourism insurance covers planned procedures and their complications-even after you return home. It includes things like revision surgery, emergency return flights, and lost deposits. They’re not the same product.

How do I know if a foreign hospital is safe?

Look for accreditation from Joint Commission International (JCI) or the Global Healthcare Accreditation (GHA) program. Check if the hospital is listed on official medical tourism portals like MedTourism.com or Health Tourism UK. Avoid clinics with no public accreditation or patient reviews.

Can I get insurance if I have a pre-existing condition?

Most medical tourism insurance policies exclude pre-existing conditions. Some providers offer limited coverage for stable conditions, but only if you’ve been cleared by your doctor and have documentation. Be upfront with the insurer-hiding a condition can void your policy.

What happens if my surgery is canceled after I book everything?

Without medical tourism insurance, you lose your deposit, flights, and hotel bookings. A good policy will refund non-refundable costs if your procedure is canceled due to medical reasons or hospital issues. Always confirm this is included before you pay.

Final Advice: Don’t Skip the Paperwork

Medical tourism isn’t illegal. It’s not even uncommon. But treating it like a vacation deal is dangerous. The savings are real-but so are the risks. The only way to protect yourself is to plan like a professional: verify the facility, buy the right insurance, document everything, and talk to your doctor before you go.If you’re considering it, start with a call to your insurer. Then call a medical tourism insurance provider. Then talk to your GP. Do this before you book a single flight. Your future self will thank you.